Target Architecture for Stress Testing (North America)

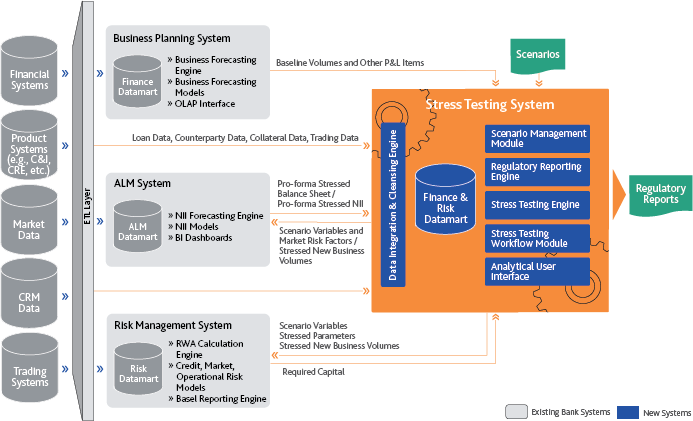

The Target Architecture for Stress Testing diagram illustrates the building blocks of a sound enterprise-wide stress testing system. The architecture highlights the need for a solution that will facilitate systems and models integration, data flow coordination, and automated reporting.

Figure 1. Target architecture for stress testing

Source: Moody's Analytics

Below is a brief description of six key elements of the architecture:

1. Data integration and cleansing engine, and finance and risk datamart

This data management platform is designed to provide the infrastructure needed to implement a world-class stress testing framework by managing and centralizing all data required for the CCAR. In preparing for the CCAR exercise, many banks struggle with pulling the necessary data from various source systems deployed for originating loans, deposits, etc. In some cases, the data is missing, forcing banks to revisit the data management process to capture the data required by the Fed.

2. Stress testing engine

The stress testing engine enables bankers to perform the calculations required to forecast expected losses, impairments, and other income and losses indicators under stress conditions. This integrated engine allows for analysis and reporting according to the scenarios put forth by the Fed as well as scenarios associated with the bank’s capital plan.

3. Scenario management module

This module enables bankers to define custom scenarios and leverage pre-defined macroeconomic scenarios, including regulatory scenarios. One hurdle many banks face is applying the economic scenarios to the market data in an integrated manner. Since the capital markets live within the economic scenarios, application of the scenarios should be included in the market data as well in order to be consistent with the economic scenarios.

4. Stress testing workflow module

This workflow includes automated software and reporting tools designed to streamline the CCAR and enterprise-wide stress testing process. Banks face a common challenge of documenting the workflow, as well as versioning and auditing the data, so that it is consistent and persistent (by associating a time series with the data).

5. Model deployment interface

This interface enables bankers to deploy the models required to conduct stress tests.

6. Regulatory reporting engine

Regulatory reporting tools streamline and facilitate regulatory and business reporting by capturing, consolidating, and reporting the data. Ideally, the tools are based on templates that reflect the requirements of the regulators. The expectation is that over time these requirements will become more complex and will require an infrastructure to support these ongoing changing rules.

Featured Experts

Juan Manuel Licari

Dr. Juan M. Licari is a managing director at Moody's Analytics. Juan and team-members are responsible for the research and analytics that enable our quantitative solutions. The team helps our customers solve complex business problems; adding value through data and analytics.

James Partridge

Credit analytics expert helping clients understand, develop, and implement credit models for origination, monitoring, and regulatory reporting.

Jamie Stark

Risk model validation consultant; product strategist; data intelligence and artificial intelligence scientist and researcher

As Published In:

Explores how North American financial institutions can leverage stress testing regulations to add value to their business, for compliance and beyond.

Previous Article

Stress Testing for Retail Credit Portfolios: A Bottom-Up ApproachRelated Articles

Final Basel III Reforms: How Can Banks Prepare for the 'Basel IV' Changes?

In finalizing its Basel III supervisory framework, the Basel Committee on Banking Supervision (BCBS) is implementing new rules for measuring credit, operational, and market risk.

IFRS 9 Survey Results

This article is a summary of the views expressed by regional banking institutions in a recent survey about IFRS 9 regulation. The survey was conducted to assess progress, potential challenges, and plans of banks with regards to IFRS 9 compliance.

Global Banking Regulatory Radar

The Moody’s Analytics Regulatory Radar provides an overview of the main regulatory guidelines affecting the banking industry. It is a proprietary tool developed to monitor regulations in the immediate, medium, and long term, across multiple jurisdictions.

Global Banking Regulatory Radar

The Global Banking Radar highlights the busy regulatory agenda that banks will face over the next couple of years. The trend of increased regulation that began in the EU and the US is now spreading to other regions, requiring banks worldwide to comply with increasingly stringent and complex requirements.

Regulatory Radar for Insurance: Emerging Regulations are Reshaping the Global Insurance Industry

The increased focus and attention on the insurance industry are illustrated by the acceleration of regulatory efforts across the globe. Keeping up with the pace of regulatory change in the current environment is one of the greatest challenges facing any insurance company.

Preparing for the Stress Tests: Regulatory Timeline and Requirements

The Moody’s Analytics Regulatory Timeline provides a high-level overview of the stress testing regulations in both the United States and European Union in the immediate and medium-term.

Stress Testing Best Practices: A Seven Steps Model

Implementing stress testing practices across the various bank divisions is a complex process. In order to address the need for an implementation framework, Moody’s Analytics has created a Seven Steps Model.

Target Architecture for Stress Testing (Europe)

The Target Architecture for Stress Testing diagram illustrates the building blocks of a sound enterprise-wide stress testing system. The architecture highlights the need for a solution that will facilitate systems and models integration, data flow coordination, and automated reporting.

Regulatory Radar

The Moody’s Analytics Regulatory Radar is a proprietary tool developed to monitor regulations in the immediate and medium term, across market segments and jurisdictions. This version provides an overview of key rules and regulatory guidelines recently published across Europe in several financial services segments.

Solvency II: A Field of Missed Opportunities?

With the Solvency II deadline approaching – full introduction of the regime is expected on 1 January 2016 and interim measures proposed by the European Insurance and Occupational Pensions Authority (EIOPA) are likely to be enforced one year earlier (i.e., in 2015) – we believe this is a timely moment to assess the progress made by industry participants toward achieving compliance and to analyze the approaches adopted by the industry to address the regulation.