Credit Transition Model

Register for the Course

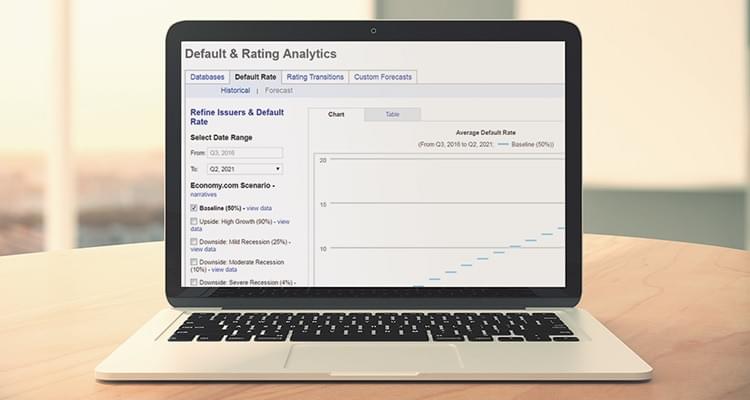

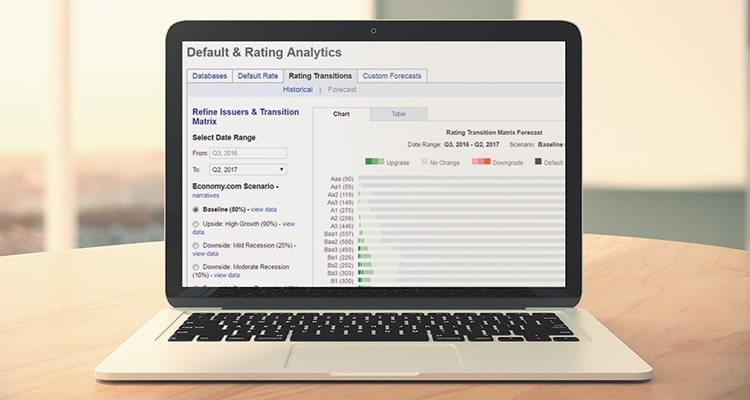

Moody's Analytics Credit Transition Model (CTM) reflects the cyclical nature of default rates and rating transitions. It incorporates macroeconomic factors that reflect the health of the economy and the market's perception of credit quality and availability.

Versatile Capabilities for Anticipating Rating Transitions and Defaults

- Supports risk assessment of specific credit default swaps (CDS), bonds, and loans.

- Calculates the expected distribution of portfolio or tranche losses as a result of either default or rating transitions.

- Allows users to calculate the probability that any specific credit will cross a predefined threshold by a particular date.

- Associates an expected time profile of default rates for an entire rating category or any particular pool of credits.

- Performs complex calculations on Moody's Analytics infrastructure and servers, allowing users to reserve processing power and resources for other needs.

Tools for Regulatory Compliance

- Easily incorporate a variety of economic assumptions into rating transition and default rate forecasts.

- Quantify how your perceptions regarding future credit risk affect your portfolio.

- Use a single trusted model to calculate default rates across multiple horizons, avoiding the contradictory forecasts often produced by multiple models, so you can better understand your risks.

- Utilize historical ratings transition patterns (including momentum) and project them forward based on economic assumptions to create sophisticated forecasts tailored to your needs.

- Systematically integrate models into your daily credit risk management practices.