Different types of businesses will require different types of help. Using a unique dataset, we assess how much and what type of financing these firms will need. Based on our analysis, restaurants will require significant help to survive, depending on the extent of the closure period. Construction companies will need help reopening.

Introduction

The coronavirus that has become widespread as of the beginning of April 2020 (COVID-19) has evolved into an unprecedented global risk and has threatened many countries. It has also cast a shadow across the entire world economy. As the pandemic has rapidly changed our societal and economic activities, with an unprecedented number of businesses shuttered for the time being, revenues drastically reduced, and historical layoffs continuing, much remains uncertain, especially the extent of financial losses.

Most small- and medium-sized enterprises have seen a substantial decline in revenues and many have been forced to close for an indefinite period. These firms will need help both surviving the period of business closure and in reopening. In this note, we estimate how much financial help they will need, and we demonstrate differences between business size and type: how much financing each will require to survive and to reopen. The help must come from many sources including banks, the government, and traditional equity investors. Assistance will likely be a mixture of methods including loans, grants, and equity infusions.

To conduct this analysis, we use a unique resource — the Credit Research Database. We have been building this financial statement database and loan payment information source in partnership with banks over the past two decades. The analysis conducted here is based on the most recent financial statements for small and medium-sized enterprises in the United States. We have excluded financial firms, real estate firms, not-for-profits, project finance, and government entities.

Methodology

Suppose a person with a history of running a successful business that was recently closed went to a bank, an investor, or a family member for a loan to survive the period of closure and to reopen. The financier would reasonably ask for a business plan that addresses two main questions: how much money per month will you need to survive the closure and how much money will you need to reopen? To project how much money is required to survive the business closure, one would start with cash on hand and then estimate the fixed costs per month as well as the variable costs that cannot be cut. For example, if the sum of these two costs is $10,000 and cash on hand is $20,000, the business can survive two months. To reopen requires financing to purchase inventory and to pay employees before revenue starts again. A retailer will probably need money to restock. If a retail shop "turns over" its inventory nine times per year, and its annual revenue is $900,000, it needs $100,000 to restock. A construction company requires additional capital to pay their employees before the firm is paid for their projects. If a construction company is typically paid every 30−60 days for "work-in-progress," and their annual revenue is $160,000 with a 25% margin, they will need $10,000−$20,000 to pay their workers and other expenses when they reopen, before being paid for the first set of projects.

To write such a business plan, the business owner must use a budget more detailed and specific than simply balance sheets, income statements, and cash flow statements. Nevertheless, by making some reasonable assumptions, we can estimate what the financing requirements would be.

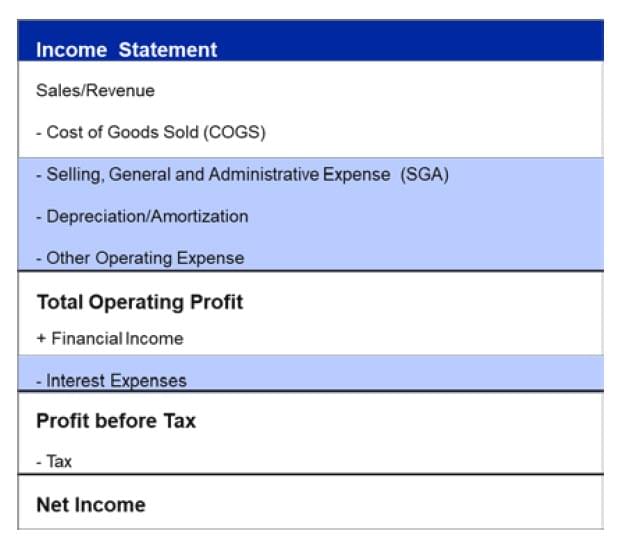

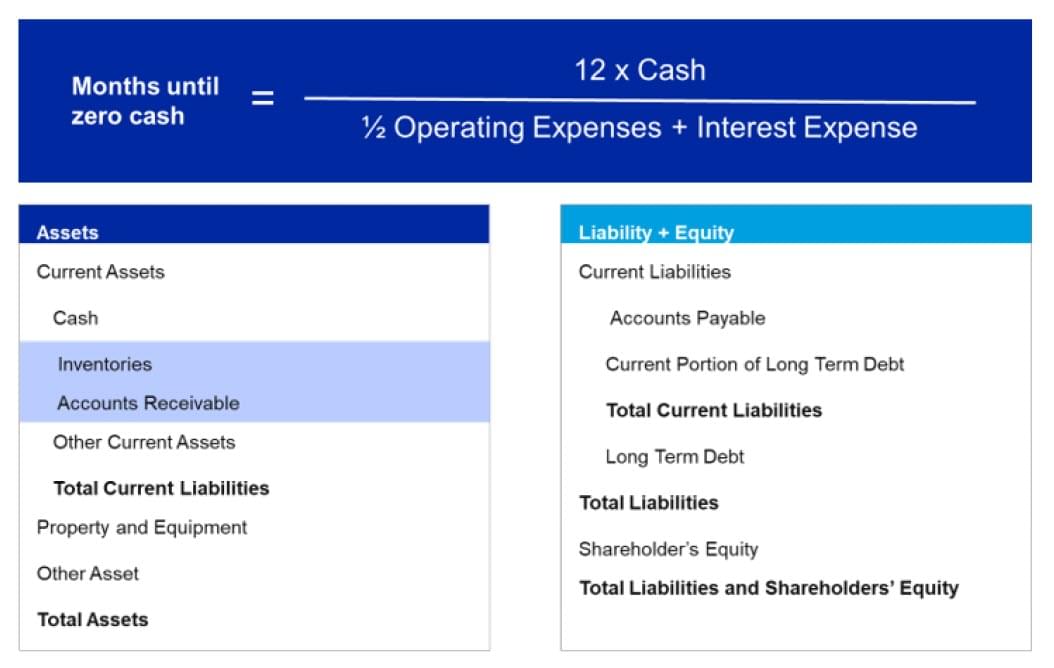

At a high level, an income statement takes Sales and subtracts "Cost of Goods Sold" to arrive at gross profit. From gross profit we subtract "Selling and General Administrative Costs" (SGA), "Depreciation and Amortization" (D&A), and "Other Operating Expenses" to arrive at "Operating Profit;" from "Operating Profit" we subtract “Interest Expense” and add back whatever “Financial Income” there is to arrive at “Profit before Tax.” Finally, taxes are subtracted to arrive at Net Income.

When a business closes, Sales declines drastically or hits zero, and Costs of Goods sold will disappear. Selling costs will largely go away, but administrative costs will not. The D&A does not go away, but it is "noncash." The cash expense associated with D&A is capital expenditures, and there will likely be some even though many businesses will seek to postpone whatever capital expenditures they can. We assume that Interest expense will need to be paid, while taxes may not be. We approximate the costs of running a closed business, as 50% of Operating Expenses (SGA + D&A + Other Operating Expense) plus Interest Expense. The 50% is a round number in the middle, that we use in the absence of a more precise alternative for this exercise — in reality, every firm differs. As this estimate is the cost per year, we divide by 12 to obtain the monthly cost. If this cost is $20,000, and cash on hand is $40,000, we estimate that the firm has two months until zero cash or two months to survive without additional aid. Further, the additional support they need to survive six months would be $80,000.

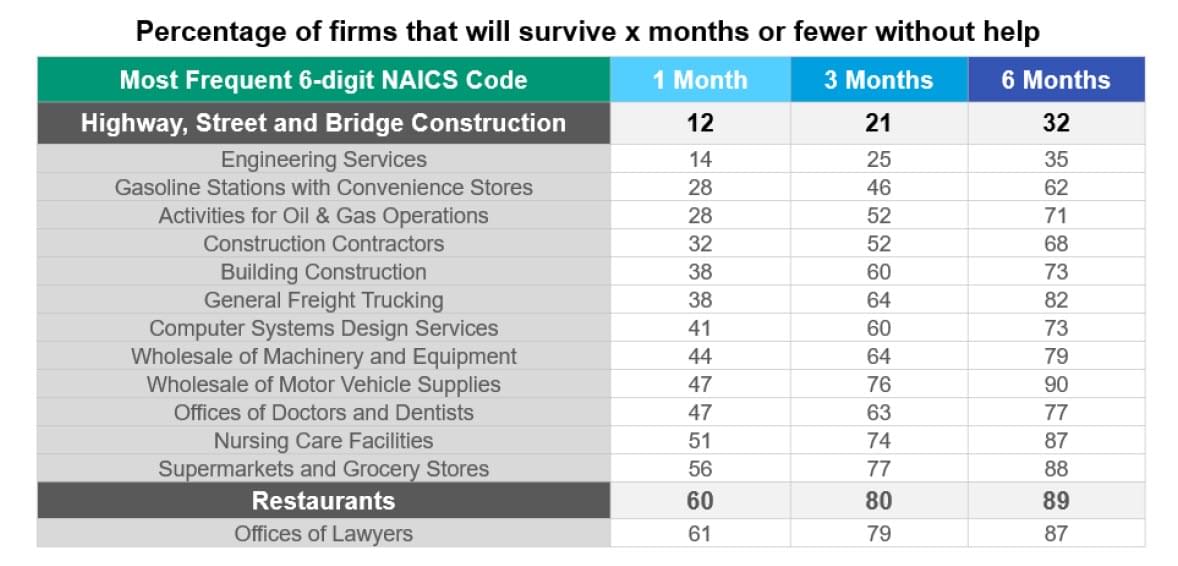

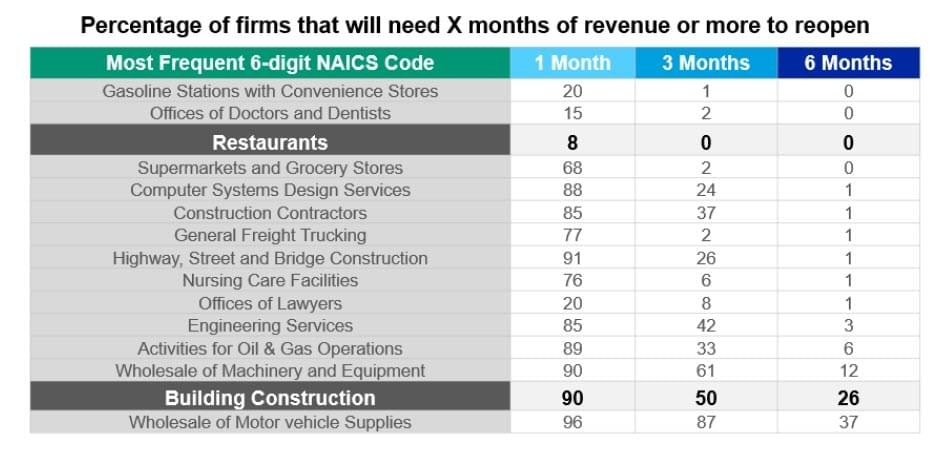

The following table shows the percentage of firms that can survive at most one month, three months, and six months, by company size. We group firms into four groups based on sales. The cutoffs are chosen such that we have about one-fourth of the firms in each group. For the smallest firms — firms with less than $4.2 million in sales — 41% will need help to survive more than one month, 62% will need help to survive three months, and 75% will need help to survive more than six months. For the largest firms with more than $80 million in sales, the situation is only somewhat better: 37% will need help to survive more than one month, 56% will need help to survive more than three months, and 70% will need help to survive more than six months.

Conclusion

Given the current environment, smaller firms will require more financial assistance to survive, as they have less cash relative to estimated fixed expenses to carry them through a closure period. Medium-sized enterprises will need more financing to reopen, as their balance sheets typically have proportionately more “non-cash current assets.” Restaurants are among the least equipped to survive a closure, but at the same time, they will need the least financing upon reopening. Builders are among the best equipped to survive a closure, but they will need the most financing upon reopening. These conclusions reflect the various business models: restaurants are paid by their customers and pay their employees frequently, whereas, builders are paid only upon completion of projects and project milestones.

Nevertheless, these results are generalized, as each firm differs, and many of the details surrounding the various plans for loans and financing small business have not yet been finalized.