Most IFRS accounting standards recognize and measure financials at the individual contract level, for example, IFRS 15 revenue from contracts and customers, and IFRS 9 financial instruments. However, insurance companies underwrite large numbers of similar contracts to pool risk. For this reason, the IASB has introduced IFRS 17 guidelines for contract aggregation for purposes of the calculation and adjustment of the Contractual Service Margin (CSM). These guidelines allow the use of a unit of account that is higher than the individual insurance contract.

The unit of account is determined by the level of aggregation, which determines the level of granularity at which onerous insurance contracts are identified and how the insurance revenue is recognized in financial statements. Therefore, the level of aggregation affects how the profitability of the business is reported. This impact on profitability is the reason why the level of aggregation in IFRS 17 is at the center of an industry debate.

This paper summarizes the aggregation requirements of the IFRS 17 standard from various perspectives, including size of groups, trend information that can be extracted from groups, degree of profitability, level of aggregation of cash flows and of CSM calculations, and risk sharing. It also includes comments from EFRAG(2018) in terms of comparing the standard to industry practices, and issues raised with the level of aggregation requirements. This document also addresses the elements that an insurance company must consider to design its own IFRS 17 grouping methodology.

Summary of requirements

The objectives of IFRS 17’s requirements for the level of aggregation are:

- Identify groups of onerous contracts as soon as possible, rather than obscure them by offsetting their losses with profitable contracts in the larger portfolio of contracts

- Avoid perpetual open portfolios

- Allocate CSM appropriately to provide accurate information about profit trends and promote systematic allocation rules over the coverage period

- Create consistency in profit recognition within the industry

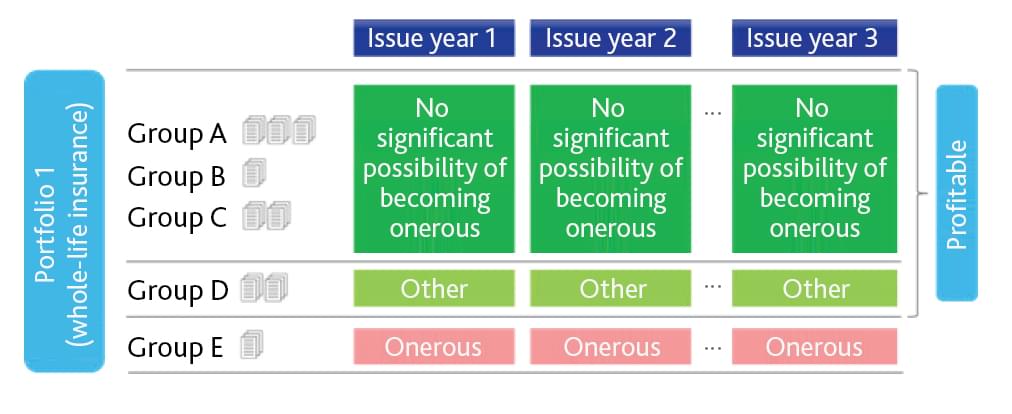

IFRS 17 requires insurers to organize insurance contracts into groups according to three criteria:

- Product portfolio

- Degree of profitability

- Year of issue

Product portfolio means contracts subject to the same risk type and managed together as a single pool. For example, contracts in the same product line – like whole life insurance, annuities, or car insurance – are expected to belong to the same portfolio.

Contracts also must be classified into groups according to the degree of profitability at initial recognition using the following criteria:

- Groups of contracts that are onerous at initial recognition

- Groups of contracts that at initial recognition have no significant possibility of becoming onerous

- Groups of remaining contracts

One of the most challenging aspects of the IFRS 17 standard, is that it requires separate reporting of onerous groups from profitable groups, which impacts when the entity must reveal these onerous groups and their total liability. If the onerous nature were revealed only by portfolio, a downward trend would likely not emerge quickly.

Groups of contracts meeting the various profitability criteria must be further split into ‘cohorts’ or ‘time buckets’ that represent an issuing period of one year or less; for example, insurance contracts issued between 22 April 20X0 and 21 April 20X1 would be split from those issued earlier or later. The rationale for the division into annual cohorts or less is that economic circumstances may change, profitability may change, or the insurer may modify the pricing of the contract. This enables identification of profitability trends and their disclosure in the financial statements. This split into time buckets, often referred to as the ‘annual cohort’ requirement, can also refer to shorter time periods, for example quarterly cohorts.

Groups are established at initial recognition and are not reassessed or modified subsequently during the coverage period. The following figure summarizes the three criteria assuming annual cohorts.

The following figure summarizes the three criteria:

Size of the group and trend information

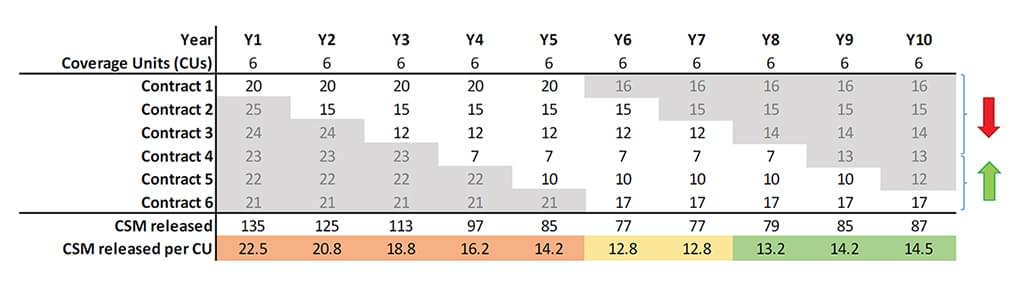

The definition of cohorts has an important role in the release of CSM to insurance revenue, since the size of the cohort will indirectly determine the amount of CSM released into revenue over time. The amount of CSM released within each reporting period is based on an average CSM per coverage unit for the group. This reflects the ratio of the service provided during the coverage period to the total projected future service until the last contract of the group matures.

For example, imagine a group with one contract with a total CSM of 100€ and contract duration of five years. If the contract represents five coverage units, the CSM will be released evenly, at a rate of 20€ each year over the coverage period1.

By adding new contracts issued each year, from year 2-6, with duration five years and one coverage unit a year, you can introduce annual cohorts that help to identify trends in profitability associated with consecutive cohorts.

The preceding table represents the overall CSM roll-forward, with in force business in gray and new business in no color. The following trend information can be detected:

- When considering individual contracts, there is a downward trend in the profitability of new contracts. For example, Contract 1 with an annual CSM release of 20 € terminates in year 6, and from that moment onward the annual CSM becomes 16€; this trend continues over the following years. Among newly written contracts, there is also the downward trend from Year 1 to Year 4, when annual CSM goes from 20 to 8. This trend is reversed starting in Year 5, when annual CSM increases from 8 to 16.

- When considering the overall CSM released per coverage unit, we can observe a downward trend form Year 1 to Year 6, and a reversal starting in Year 8.

Without annual cohorts, and with a higher level of aggregation, the trends described in point a) would not be identified and the only information extracted from the CSM release would be trend b).

Degree of profitability and size of groups of contracts

Contracts are considered onerous at initial recognition, if the fulfillment cash flow arising from the contract is a net outflow2. In this case, the insurer recognizes an immediate loss in the financial statements and a CSM of zero is established. The assessment to determine if a contract that is not onerous has no significant possibility of becoming onerous can be based on the sensitivity of the profit to the assumptions used (which calls for some judgment) and on internal reporting information. The objective, however, is to ensure that contracts are separated into groups that are initially onerous, and contracts that could join the onerous group at a future date, so that there is reasonably prompt recognition of losses on onerous contracts within each issue year cohort.

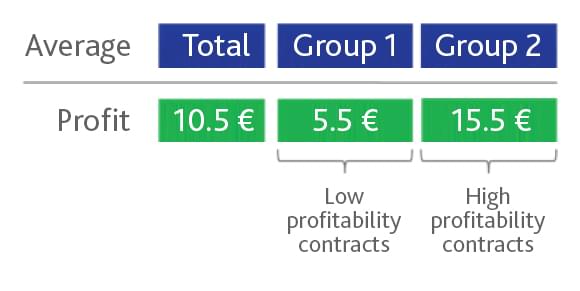

If contracts are not onerous, they are considered profitable, even if different groups will have different levels of profitability. For example, following EFRAG (2018), we assume an insurer issues 20 contracts. For simplicity, we assume each contract contains one coverage unit each. These contracts contribute CSM at recognition ranging from 1€ to 20 €. They are aggregated into Group 1, which contributes CSM from 1€ to 10€, and Group 2 which contributes CSM from 11€ to 20€. The average CSM per coverage unit will be the following:

Working with averages allows us to avoid calculating CSM balances and releases on contract-level de-recognition. For example, if a contract is derecognized earlier than expected, working at contract level would require us to modify the CSM by adjusting the fulfillment cash flows of the specific contract. Since individual contract CSM calculation and reporting is operationally costly, the standard allows for grouping. Grouping allows us to de-recognize the contract from the CSM by using an average at the moment of the de-recognition.

Logically, the average CSM at the portfolio level is different from the CSM of the individual contracts. For example, assume that we need to derecognize a contract with CSM 2€. If we work with a portfolio average, we would need to consider an average of 10.5€ which is significantly higher than the contract CSM. Conversely, if we work with groups with high and low profitability, the contract level CSM (2€) will be closer to the CSM average of low profitability group (5.5€). Therefore, tracking profitability of the three standard groups allows us to track profitability more closely to the CSM contract-level amounts, without incurring in the operational costs of individual tracking. Moreover, working with groups allows us to avoid a situation where contracts with low profitability that are likely to become onerous are mixed with contracts with high profitability. This combination makes the overall profitability assessment more diluted and opaque.

At a minimum, an insurer must divide contracts in the three regulatory groups explained in the preceding section, but the insurer can also opt for a larger number of groups reflecting different levels of profitability. The key advantage of such level of aggregation is the possibility to spot and track information about profitability trends that at a higher level of aggregation would be lost. The standard explicitly permits that a proposed grouping may be assessed for profitability level by analysis of the set of new contracts assigned to the group as a whole, if there is sufficient supporting information that enables us to conclude that the contracts should belong to the same group. Otherwise the contracts’ profitability should be assessed one by one to assign to appropriate groups. In practice, the number of these groups and how to define them is at the center of a debate.

Finally, laws or regulation may mandate a pricing structure that does not reflect the economic characteristics of the contract. In this case, the standard allows insurers, as an exception, to place contracts in the same group that normally would be distributed in different groups. For example, consider two sets of contracts A and B, with similar risks and managed together, and where policyholders of set B have higher risk characteristics. If policyholders of set B are charged a higher premium, then the contract may be profitable. Conversely, if they are charged the same premiums as set A, there is the possibility that the contracts will be onerous, so they will need to be allocated to different groups. If, however, regulation restricts the insurer to charge for set B the same premiums of set A, then the two sets of contracts can be placed in the same group.

Level of aggregation of cash flows and of CSM

In IFRS 17, profits arising from future service are treated differently from losses. Profits arising from future service are recognized over the coverage period, while losses are recognized when they are identified.

The standard suggests estimating fulfillment cash flows at whatever level of aggregation is more appropriate. This leaves open the possibility to model them at aggregated level or at contract level. These different treatments and the flexibility allowed by the standard, enable companies to have a significant degree of freedom in terms of level of aggregation, and to adopt different levels of granularity for fulfillment cash flows and CSM calculations.

In terms of level of aggregation for CSM calculations, most of the companies we observe have decided to perform calculations according to the minimum granularity required by the standard, which is portfolios, onerous assessment, and annual cohorts.

In terms of level of granularity of the fulfillment cash flows, we have observed the following trends:

- The contract grouping used for Solvency II will not work for IFRS 17, therefore a new grouping policy must be put in place. Often the new level of grouping involves not only a methodological decision, but also problems of data quality, like missing data.

- Companies that aim for minimal compliance will try to minimize the operational costs associated with finer granularity. They will look at a level of granularity in the grouping of cash flows that is consistent with level of aggregation requirements for CSM, that is according to the degree of profitability.

- Companies with heterogeneous actuarial systems, often receive cash flow with heterogeneous granularities. They may consider their IFRS 17 project to be an opportunity to implement a more granular and homogeneous3 level of cash flows across the various entities of the group. In this case, they are likely to pursue granularity that is as fine as possible.

- We have observed companies targeting policy level fulfillment cash flows. This option is most consistent with principles-based approaches based on gross premium valuation, since individual contract calculations are much more sensitive to individual contract differences than model point approaches, and therefore the results they return are more accurate.

- Companies that have implemented their accounting systems at the policy level, which is rare, will also be able to use such level of granularity.

Companies are currently seeking systems and expertise to support IFRS 17 calculations including specifically the CSM. We believe the tools required to investigate and address these issues should be:

- Agnostic to the underlying valuation systems and accept range of inputs

- Allow reconciliations to the groupings used for other reporting purposes

- Facilitate easy process management so that multiple runs can be carried out to investigate different grouping strategies

- Able to support policy level calculations, if required

- Provide insightful output to support determination of the optimal strategy, including considering alternative future outcomes

Risk sharing in IFRS 17

IFRS 17 refers to risk pooling as risk sharing, meaning that many policyholders act together as a loss absorbing buffer against the occurrence of an adverse event. IFRS 17 risk sharing refers to the case when an insurance contract in one group includes conditions that affect the cash flows of policyholders in a different group (B67-71)4. Take, for example, two policyholders that share the same pool of underlying assets, but A has a minimum guaranteed of 7% and B has a minimum guaranteed of 2%. If the return from the pool of underlying assets is 5%, A will receive 7% as per the contract (2% more than the effective fund return), while B will receive the residual return of 3% (1% more than the contractual minimum, but 2% less the effective fund return). The payout to A is increased, while the payout to B is reduced. Hence, the two contracts are interdependent, and B absorbs a loss for the benefit of A policyholders.

For IFRS 17, risk sharing occurs when contracts that are interdependent in terms of cash flows belong to different units of account or groups. In this case the estimated cash flows should also consider cash transfer between groups.

Issues with level of aggregation

The following issues were raised by EFRAG (2018), a consultation paper published to promote a debate across the industry5. The first issue raised is the annual cohort requirement. Splitting an insurance product with a life span of, for example, ten years means significantly multiplying the number of groups, which bears an extra operational cost in terms systems updates and changes. The proliferation of the number of groups creates data management issues, having to store CSM balances by group, permanently retain group assignment, and manage the demanding roll-forward process by group.

The current accounting practice monitors profitability at a higher level of aggregation. This is in part due to IFRS 4, which allows for greater flexibility in terms of unit of account. To make things more challenging, we must also consider that under the previous standard different elements of the financial statement can use different units of account and the practice varies from one company to another. Furthermore, companies may use different levels of aggregation in different internal processes, for example product design and pricing, risk assessment, monitoring and reporting.

IFRS 17 has provided a new model for identifying onerous contracts. Before, contracts were grouped in a larger pool to calculate profitability. Now losses cannot be diluted in a large pool, they must be made explicit when they are recognized. For example, consider an insurance company selling two insurance contracts, one with characteristic X, and one without it. If X is included, the contract is onerous at 50 €, while if X is excluded, the contract is profitable at 200€ over the coverage period. If measured individually, loss is recognized immediately, while if measured together, over the coverage period the profit will still be 150 €. However, a lesser amount of useful information is collected with this set of contracts, and the loss information is captured gradually over the coverage period rather than immediately. The introduction of the notion of onerous contract may also affect the pricing of some contracts since the timing of reported earnings will be impacted.

The split of mutualized amounts into groups of contracts is seen by EFRAG as artificial and divergent from current practices. IFRS 17 does not use the term “mutualization”, it refers instead to “risk sharing.” In practice, according to EFRAG, the term encompasses a larger number of effects, such as individual contract requirements, risk diversification, and cross-subsidization. EFRAG therefore suggests considering mutualization in the determination of the insurance groups.

Current practice in the insurance industry leverages the use of open portfolios, where contracts are added and removed continuously from an insurance group. As shown above, one of the IFRS 17 goals is to avoid perpetually open portfolios.

Conclusions

The level of aggregation of CSM calculations should reflect the true economic nature of the underlying groups of insurance contracts. At the same time, granularity that is too detailed may introduce noise and increase complexity in terms of data volumes. The level of aggregation should be designed according to the data available, and associated to the characteristics of the policies that will make the analytics meaningful over the final CSM results. In conclusion, the optimal level of aggregation of CSM calculations depends on the types of insurance policies and availability of data to produce useful analytics of contract groups.

The debate in the industry is animated, fueled by initiatives like EFRAG (2018). As insurance companies embark upon CSM implementations, we believe that best practices will emerge in terms of methodology for level of aggregation, providing guidelines that can be adopted by the whole industry.

EFRAG (2017), “EFRAG TEG - Educational Session“, 23 November 2017, Agenda paper 03-05

EFRAG (2018), “ IFRS 17 Insurance Contracts and Level of Aggregation, A background briefing paper“,23/02/2018,http://www.efrag. org/News/Project-307/EFRAG-issues-IFRS-17-background-briefing-paper-on-level-of-aggregation

IFRS (2017), “IFRS 17 Insurance Contracts”, May 2017, https://www.idc.ac.il/he/specialprograms/accounting/fvf/Documents/IFRS17/ WEBSITE155.pdf

IFRS (2018), “IFRS 17 webcast: Level of aggregation”, 18 January 2018, http://www.ifrs.org/news-and-events/2018/01/ new-ifrs-17-webcast-level-of-aggregation/

1 The even release of the CSM over the coverage period is a simplification, especially for contracts that have a probability of being terminated by claim or by policyholder lapse. The standard allows the projection of expected coverage units over the contract period with the expectation that service delivered decreases steadily over time. With average lapse rates of 10 to 15% or more in early years and termination rates increasing by age to a high amount in later years, the decrease will not be linear like in this example. A more realistic example would assume a regular 5 / 10% lapse rate.

2 A simplification is provided in IFRS 17, Paragraph 47 for the Premium Allocation Approach (PAA) methodology: an entity can assume that no contracts are onerous at initial recognition, unless facts and circumstances indicate otherwise. The entity will have to assess whether contracts belong to the two remaining groups based on likelihood of changes in these facts or circumstances.

3 Homogeneous granularity enables firms to provide a common data structure across group entities to the CSM calculations, which lowers project complexity and risk.

4 The example in this section does not apply to reinsurance contracts.

5 EFRAG (2018) p. 5.