Accounting for Purchased Credit Deteriorated Financial Assets: Current and Future GAAP

The current expected credit loss (CECL) model is expected to fix the delayed recognition of credit losses and provide a uniform approach for reserving against credit losses on all financial assets measured at amortized cost. However, CECL introduces new complexities. In this article, we explore existing and future accounting and operational challenges faced by institutions acquiring financial assets with credit deterioration.

The Financial Accounting Standards Board (FASB) has historically recognized that collectability of contractual amounts is a crucial piece of financial information for investors to consider when making lending decisions. Current Generally Accepted Accounting Principles (GAAP) set by the FASB address impairment accounting by creditors by consistently incorporating concepts related to contractually required payments receivable, initial investment, and cash flows expected to be collected (see Accounting Standard Codification (ASC) Topic 310 – Receivables). Introduced in December 2003, purchased credit impaired (PCI) accounting requires entities to implement a complex accounting treatment of income and impairment recognition for PCI assets1 where expectation of collectability is reflected in both purchase price and future expectations of cash flows, while contractual cash flows are ignored. Since adoption, entities struggled with operational challenges, income volatility, and comparability of PCI versus originated assets accounting.

The current expected credit loss (CECL) model, taking effect in 2020 for public business entities that are SEC filers, attempts to align measurement of credit losses for all financial assets held at amortized cost and specifically calls out potential improvements to the accounting for PCI assets. CECL changes the scope by introducing the concept of purchased credit deteriorated (PCD) financial assets and makes the computation of the allowance for credit losses for PCDs, as well as recognition of interest income, more comparable with the originated assets.

In this article, we will focus on changes in the accounting for loans2 with evidence of deterioration of credit quality since origination. We will also explore potential complexities which remain despite the attempt to align the accounting for purchased and originated assets.

Definitions and Scope

To understand how CECL changes the accounting for purchased loans, it is important to start with definitions. According to the current GAAP, PCI loans are loans that:

- Are acquired by the completion of a transfer.

- Exhibit evidence of credit quality deterioration since origination.

- Meet a probability threshold, which indicates that upon acquisition, it is probable the investor will be unable to collect all contractually required payments receivable.

Accurately defining which acquired assets should be considered PCI presents an operational challenge, given the often inadequate amount of data available to the acquirer at the time of acquisition. While being conservative, entities end up scoping in assets that, over their remaining life, significantly outperform the expectation and for which all contractually required cash flows are subsequently collected. Once an asset is designated as a PCI, it remains a PCI regardless of its performance (unless it is modified as a troubled debt restructuring). Most core banking systems are not set up to handle special accounting based on expected cash flows, causing financial institutions to implement systems and processes on top of what is used for the originated book.

CECL, which completely supersedes current accounting for PCI financial assets, continues to require different treatment at initial recognition for purchased loans with evidence of credit quality deterioration, and defines PCD assets as:

- “Acquired individual financial assets (or acquired groups of financial assets with similar risk characteristics) that,

- As of the date of acquisition, have experienced a more-than-insignificant deterioration in credit quality since origination, as determined by an acquirer’s assessment.”

Compared to the current GAAP, CECL changes the scope by adding the more-than-insignificant criterion and removing the probability threshold. Identifying PCD assets will most likely continue to present an operational challenge when defining more-than-insignificant deterioration. The FASB suggests considering multiple qualitative factors,3 and the abilities to systematically consume large amounts of data points, apply data rules, and appropriately tag the acquired assets are key in accurate PCD designation.

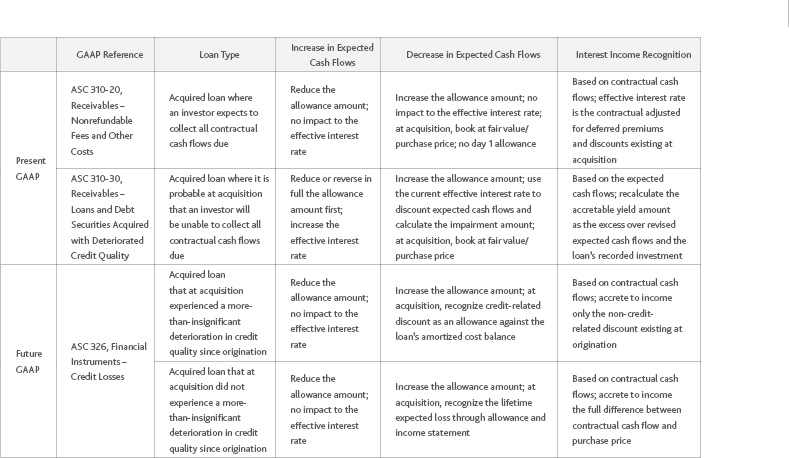

How does PCD designation affect the financials at acquisition and beyond? To demonstrate, Figure 1 summarizes the basis of accounting for the acquired loans under current and future GAAP and reviews changes to day 1 and day 2 accounting requirements.

Figure 1 Comparison of current and future GAAP for PCD assets

Source: FASB

Changes to Day 1 Accounting

On day 1 (at acquisition or origination), CECL requires firms to measure the credit losses for newly recognized financial assets. The allowance for credit losses is recorded to present the net amount expected to be collected on the balance sheet. For non-PCD assets, credit loss expense is recorded on the income statement to establish the allowance; the difference between the purchase price and loan receivable is amortized over the remaining life of the loan.

For PCD assets, there is no income statement impact on day 1: The initial allowance for credit losses is added to the purchase price and is considered to be part of the PCD loan amortized cost basis. The loan-level non-credit-related discount is derived from the difference between the receivable and amortized cost, and amortized over the remaining life of the PCD asset. Note that GAAP presents an interesting misalignment between PCDs and all other financial assets carried at amortized cost: origination or acquisition of non-PCD assets that are less risky than PCD by definition results in a recording of a lifetime loss through the income statement while acquisition of PCDs impacts the balance sheet only.

A circularity concern arises when including allowance for credit losses in the PCD’s amortized cost, where allowance may not be measured until amortized cost is known. (Similarly, when the discounted cash flow approach is used, effective interest rate determination gives rise to a circularity issue where such a rate cannot be determined until the discounted rate is determined.) To avoid this, the FASB provided additional guidance for amortized cost basis and effective interest rate calculation. When the discounted cash flow methodology is used, the expected credit losses (ECLs) are discounted at the rate that equates future expected cash flows with the purchase price. When other methodologies are used to calculate ECL, the allowance is based on the unpaid principal balance of the loan.

Under the current GAAP, it is not appropriate to record a loss allowance at acquisition, and the acquired loan is recorded at its purchase price. For loans acquired in a business combination, the initial recognition of those loans is based on the present value of amounts expected to be received. Allowance for credit losses for the PCI loans reflects only those losses that are incurred by the investor after acquisition. The difference between gross expected cash flows and contractual cash flows over the life of the loan represents a nonaccretable difference, which is disclosed at acquisition in the financial statement footnotes but not on the balance sheet. The difference between PCI loan purchase price and gross expected cash flows is accreted to income over the life of the loan using effective interest rate (accretable yield amount).

Let’s use a simple example to demonstrate the differences in day 1 and day 2 accounting for PCD and PCI. Assume that an entity acquired a fixed-rate loan for $60 with a coupon monthly rate of 3%, par balance of $100, and a five-month remaining contractual life with no expectation of prepayment. The contractual amortization schedule is presented in Figure 2.

Figure 2 Contractual amortization schedule for a sample loan

Source: Moody's Analytics

Under PCI accounting (current GAAP), an entity will make the following day 1 entry to record the loan purchase at its fair value, with DR representing a debit amount and CR representing credit:

Unlike the current standard, CECL does not require a discounted cash flow methodology for PCD assets. However, to compare PCI and PCD accounting, we will use the discounted cash flow methodology to calculate ECL. To determine the allowance for credit losses on day 1 for the PCD loan using this methodology, ECLs are discounted at the rate that equates net present value of the future expected cash flows with the purchase price. We will assume the cash flow stream shown in Figure 3 over the life of the asset, taking into consideration past events, current conditions, and reasonable and supportable forward-looking information.

Figure 3 Sample cash flow stream

Source: Moody's Analytics

To record the day 1 allowance for credit losses for this PCD loan, we need to calculate the discount rate that equates the expected cash flows with the purchase price of the asset. This required discount rate is 5.63%. Allowance for the credit losses equals the net present value of the expected cash flows lost discounted by 5.63%, that is $32.92. To determine the initial amortized cost for the PCD asset, an entity has to add the allowance amount to the purchase price. The remaining difference between the loan receivable and PCD loan amortized cost is the non-credit-related discount that has to be tracked for amortization purposes from day 1.

As demonstrated, PCD accounting will continue to present an operational challenge for entities due to the requirement to calculate, track, and amortize loan-level non-credit-related discounts.

Changes to Day 2 Accounting

After acquisition, recognition of income and expected losses under current and future GAAP also differs.

CECL PCD accounting for interest income recognition is consistent with non-PCD acquired or originated loan accounting, except for the treatment of the day 1 purchase discount. The day 1 discount attributable to credit losses is not amortized into income, which is achieved by adding it to the day 1 amortized cost. Interest income for PCD loans is recognized similar to originated assets based on contractual cash flows where the non-credit-related discount is amortized over the remaining life of the loan. Note that the discount rate used to calculate day 1 allowance under the discounted cash low methodology is the same as the effective interest rate4 that would be used to recognize interest income on the PCD loan.5

Using our example, the amortization schedule for the PCD loan is shown in Figure 4, and the period 1 interest income recognition journal entry is as follows:

Figure 4 Amortization schedule for a PCD loan

Source: Moody's Analytics

PCI accounting for interest income recognition is complex and based on the expected cash flow changes over time. It requires effective interest rate recalculations as the cash flow expectations improve over time. A Statement of Position released by the FASB states:

“If, upon subsequent evaluation… based on current information and events, it is probable that there is a significant increase in cash flows previously expected to be collected or if actual cash flows are significantly greater than cash flows previously expected, the investor should:

- Reduce any remaining valuation (or allowance for loan losses) for the loan established after its acquisition for the increase in the present value of cash flows expected to be collected, and

- Recalculate the amount of accretable yield for the loan as the excess of the revised cash flows expected to be collected over the sum of (a) the initial investment less (b) cash collected less (c) write-downs plus (d) amount of yield accreted to date.”

The FASB also instructs, “The investor should adjust the amount of accretable yield by reclassification from nonaccretable difference.” The resulting yield is used as the effective interest rate in any subsequent application, including the calculation of the future impairment amount. The amount of accretion is tied to the future expectations of cash flows, while contractual cash flows are ignored. PCI accounting, applied to performing assets that were, perhaps erroneously, designated as PCIs at acquisition, often results in unusually high effective yields as well as unreasonable impairment amounts when a decrease in expected cash flows triggers discounting with such yields.

Figure 5 Day 1 accretion schedule for a PCI loan

Source: Moody's Analytics

For simplicity, we will assume that the expected cash flows for the PCI loan are the same as for PCD in our example. The day 1 accretion schedule is shown in Figure 5, and the period 1 interest income recognition journal entry is as follows:

Neither standard considers it appropriate to record into income amounts that are not expected to be collected at acquisition. While current GAAP establishes a nonaccretable difference for PCI assets outside of financial statements, CECL includes a credit-related discount into amortized cost for PCDs. Neither standard allows recognition of interest income, to the extent that the net investment in the financial asset would increase to an amount greater than the payoff amount.

The FASB decided that purchased assets and originated assets should follow the same accounting model approach to the extent possible. Consequently, other than applying a “gross-up approach” for the PCD assets (i.e., including day 1 allowance in the amortized cost basis), estimation of the expected credit losses for PCD assets follows the same methodology as originated assets under CECL. Allowance method is not prescribed (i.e., discounted cash flow approach is not required for PCD loans6). An investor has to estimate credit losses over the contractual term of the financial asset, consider even a remote probability of a loss, and incorporate information on past events, current conditions, and reasonable and supportable forecasts. Furthermore, the loss estimate should be based on point-in-time measures, reflecting the entity’s current environment and the instrument’s “position” in the economic cycle rather than average-based, through-the-cycle measures.

An investor has to estimate credit losses over the contractual term of the financial asset, consider even a remote probability of a loss, and incorporate information on past events, current conditions, and reasonable and supportable forecasts.

Current GAAP states that an investor should continue to estimate cash flows expected to be collected over the life of the PCI loan. A PCI loan is considered impaired “if, upon subsequent evaluation based on current information and events, it is probable that the investor is unable to collect all cash flows expected at acquisition plus additional cash flows expected to be collected arising from changes in estimate after acquisition.”

That is, if a PCI asset is not impaired, then no additional reserve is booked or an existing allowance is reversed. Entities are required to use discounted cash flow methodology to estimate expected credit losses on the PCI loans. The impairment amount is calculated by comparing the loan’s recorded investment with the net present value of remaining expected cash flows discounted at the effective interest rate. The loan’s recorded investment is defined as the sum of the loan’s fair value on day 1 adjusted for accumulated accretion, plus payments and charge-offs to date. The day 2 PCI allowance is booked through income statement provision for credit losses.

Based on these outlined requirements, it is clear that the loss estimate would change for the same loan even if the same loss estimate methodology (e.g., discounted cash flow approach) is used. Removal of the probability threshold/requirement for impairment and incorporation of forward-looking information are primary reasons for the expected difference.

Let’s continue using our example and assume that in the first period, instead of receiving $10.00 of expected cash flows, we received only $7.00. Let’s also assume that our future cash flow expectation or contractual life does not change.

Figure 6 Amortization under PCI, based on excess cash flow (ECF)

Source: Moody's Analytics

Under PCI accounting, the loan will be impaired as actual cash flows were below expected. The impairment will be calculated by discounting the remaining expected cash flows using the existing effective interest rate of 5.63%. We compare this net present value of $53.40 to the recorded investment of $56.40 (day 1 carrying amount of $60.00 plus accretion of $3.40 minus payment of $7.00), resulting in a $3.00 allowance amount. See the updated accretion schedule for this PCI loan in Figure 6. Note that the accretion income is booked based on the carrying value of $53.40 (recorded investment net of allowance amount) going forward.

For the PCD loan under CECL, day 2 allowance calculations are consistent with the CECL discounted cash flow methodology as follows. Net present value of the expected cash flows ($53.40) is compared to the amortized cost of $90.26 as of the second reporting period; see Figure 7, where this PCD loan’s amortization schedule is recalculated based on a new required contractual payment. The day 2 allowance equals $36.86. The amortized cost amount already includes the day 1 allowance of $32.92 due to the gross-up approach. Thus, an additional provision expense of $3.94 is booked for the difference between day 2 and day 1 allowance amounts.

Figure 7 PCD loan’s amortization schedule recalculated based on a new required contractual payment

Source: Moody's Analytics

Note that due to the receipt of the less-than-expected payment, too much income was recognized for the first period, and the discount amortization is adjusted from $2.23 down to $1.34. Consequently, a catch-up journal entry is recorded to adjust the remaining unamortized balance of the non-credit-related discount against interest income:

Conclusion

As entities transition to CECL,7 we expect that certain PCD accounting operational difficulties will continue to exist due to allocation and amortization of the non-credit-related discount at the individual asset level. CECL closely aligns credit loss measurement methodologies across originated and purchased portfolios and provides for consistent income recognition models based on contractual cash flows. However, the introduction of the lifetime loss estimate, including the incorporation of forward-looking information, demands significant improvements in entities’ data collection, accessibility, and retention capabilities, as well as more granular and potentially more sophisticated loss measurement methodologies and analytics and reporting.

Sources

1 See FASB, “Statement of Position 03-3: Accounting for Certain Loans and Debt Securities Acquired in a Transfer,” and FASB, “ASC 310-30, Receivables – Loans and Debt Securities Acquired With Deteriorated Credit Quality.”

2 CECL changes the accounting for other PCD assets, including debt securities, which are not in scope for this article.

3 See ASC Topic 326, paragraphs 326-20-55-58 and 326-20-55-4.

4 As defined in ASC Topic 326, effective interest rate is “the rate of return implicit in the financial asset, that is, the contractual interest rate adjusted for any net deferred fees or costs, premium, or discount existing at the origination or acquisition of the financial asset.”

5 PCI accounting allows loans to be aggregated into a pool if they are not accounted for as debt securities, are acquired in the same fiscal quarter, and have common risk characteristics. The pooled loans can then use a composite interest rate and expectation of cash flows expected to be collected for that pool. Once a pool is assembled, its integrity is maintained for purposes of applying the recognition, measurement, and disclosure provisions of PCI accounting. CECL does not provide for the PCD pool accounting (due to individual allocation of the non-credit-related discount) but allows for the maintenance of existing pools upon the transition from PCI to PCD. Pool accounting is outside the scope of this article, which focuses on individually accounted PCI and PCD loans.

6 There are certain additional requirements when discounted cash flow methodologies are used to calculate the discount rate, as well as a different basis for calculation when other methods are utilized. See ASC Topic 326, paragraphs 326-20-30-13 and 326-20-30-14.

7 Upon CECL adoption, entities will not be required to retrospectively reassess whether their existing PCI assets meet the definition of PCD. Rather, they will adjust the amortized cost basis of the PCI assets to reflect the addition of the allowance and begin accreting into income the non-credit-related discount after the adjustment to the amortized cost basis using the interest method based on the effective interest rate.

Featured Experts

Scott Dietz

Scott is a Director in the Regulatory and Accounting Solutions team responsible for providing accounting expertise across solutions, products, and services offered by Moody’s Analytics in the US. He has over 15 years of experience leading auditing, consulting and accounting policy initiatives for financial institutions.

Laurent Birade

Advises U.S. and Canadian financial institutions on risk and finance integration, CCAR/DFAST stress testing, IFRS9 and CECL credit loss reserving, and credit risk practices.

James Partridge

Credit analytics expert helping clients understand, develop, and implement credit models for origination, monitoring, and regulatory reporting.

As Published In:

Examines the role of disruptive technologies in the financial sector and how firms can improve their practices to remain competitive.

Previous Article

Predicting Earnings: CECL’s Implications for Allowance ForecastsRelated Articles

Managing an Insurance Company's Credit Portfolio Through COVID-19

The COVID-19 pandemic has brought credit risks that are unprecedented in size, are fast-changing, and have vastly different manifestations across industries. The uncertainty of impact is driven by epidemiological progression and sociological response, balanced by fiscal and monetary stimulus.

Concentration Risk Consideration During the Allowance Process and COVID-19's Impact

COVID-19 created additional complexities for institutions navigating CECL accounting standard. This paper provides a natural quantitative approach for incorporating concentration in the allowance process and portfolio management.

Moody's Analytics Webinar: Reinsurance Receivables under CECL

This webinar will focus on the implementation considerations and challenges of the CECL accounting standards for insurers.

Reinsurance Receivables Under CECL

For insurers, including reinsurance receivables is a unique result of the CECL accounting standard.

Moody's Analytics Webinar: CECL Considerations for Insurers - AFS Debt Securities and Other Assets

The CECL accounting standard affects a broad spectrum of financial institutions, including insurers. Investment portfolios may require updates to allow expected credit loss calculations. Understand the impact of CECL on debt securities, commercial real estate (CRE) loans, and operations, and discover potential solutions.

CECL Considerations for Insurers - AFS Debt Securities and Other Assets

The CECL accounting standard affects a broad spectrum of financial institutions, including insurers. Investment portfolios may require updates to allow expected credit loss calculations. Understand the impact of CECL on debt securities, commercial real estate (CRE) loans, and operations, and discover potential solutions.

Moody's Analytics Webinar: Acquisition Accounting Under CECL

Join our experts as they discuss the effects of CECL on acquisition accounting, including PCD accounting, and the possible ramifications to the acquisition market.

Acquisition Accounting Under CECL

Join our experts as they discuss the effects of CECL on acquisition accounting, including PCD accounting, and the possible ramifications to the acquisition market.

The Impact of Assumptions on the CECL Estimate

Across institutions of all sizes, one of the questions executive management should be asking their CECL working groups is, "What is the impact to our bottom line?"

Moody's Analytics Webinar: CECL Disclosures – Required and Beyond

Based on the required disclosures for CECL, discuss what readers of your financial statements will be able to do and what type of additional information they would expect. We will cover potential implication of the methodology chosen to the expected disclosures.